We are currently in the last quarter of FY 2023–24 / AY 2024–25. For Assessment Year 2024–25 (FY 2023–24), tax preparation can still be undertaken at any time; January and February of 2024 are still good starting months. Under Section 80C of the Income Tax Act of 1961, taxpayers may deduct up to Rs 150,000 from their taxable income by investing in specific eligible instruments. These products include mutual funds, Equity Linked Savings Schemes (ELSS), Public Provident Funds (PPF), Employee and Voluntary Provident Funds (EPF and VPF), National Savings Certificates (NSC), tax-saving bank fixed deposits with a 5-year lock-in period, and both standard and unit-linked life insurance policies.

Why is it crucial to plan while filing your taxes?

You can file your income tax returns under one of the two tax regimes: the Old Tax Regime or the New Tax Regime. There are reduced tax rates for various income groups under Rs 15 lakhs under the New Tax Regime. However, there are no deductions allowed under the New Tax Regimes. On the other hand, under the Old Tax Regime, payments for investments made under Section 80C as well as under several other sections of the Income Tax Act, including Section 24 about interest on home loans and Sections 80CCD (NPS) and 80D (health insurance) may be written off. If any of these deductions apply to you, you may find that the Old Tax Regime benefits you more than it does. You must start your tax preparation as soon as possible to give yourself enough time to evaluate different scenarios and, after consulting with your tax expert, make well-informed decisions. It would help if you also give yourself ample time before making your 80C investments so that you can gather the required resources. Another argument in favor of planning your taxes well in advance.

What is the best way to handle tax planning for 80C investments?

Under section 80C, the maximum amount that can be deducted is Rs 150,000, regardless of income tax slabs.

Section 80C would allow for the deduction of salaried investors’ contributions to the Employee Provident Fund (EPF).

If you are making EMI instalments for a house loan, the principal amount of the payments for the year will also be mentioned.

You will be reimbursed for the annual premium for any life insurance policies you may hold.

Ascertain the complete amount of investment necessary to obtain the full benefit under Section 80C and the whole amount of the above-mentioned deductions for which you qualify.

When selecting an 80C plan for tax-saving investments, consider your risk tolerance and financial goals.

If you want to save taxes and build wealth at the same time, and you have a high-risk tolerance, ELSS may be an excellent 80C tax-saving option.

ELSS: What is it?

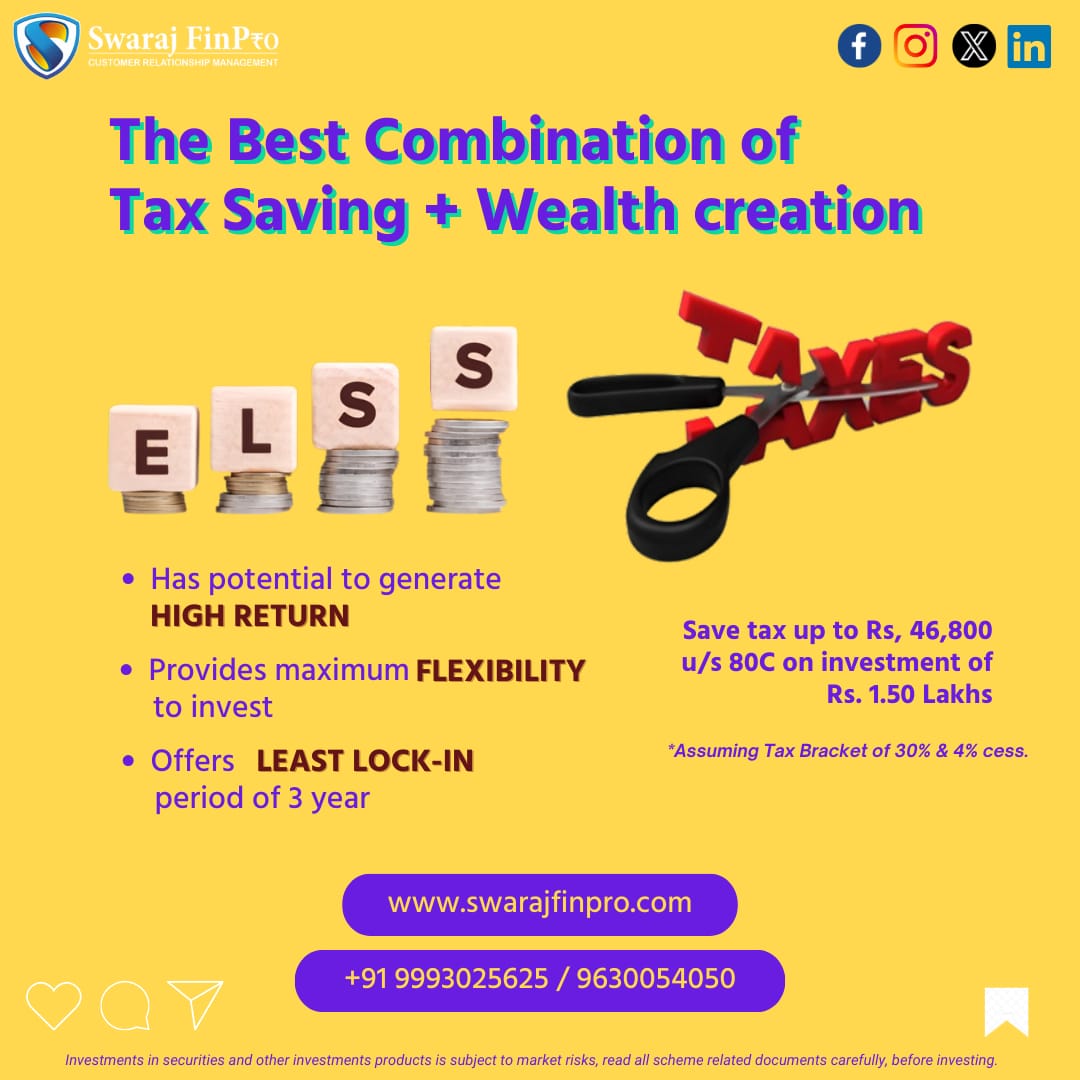

Equity-linked savings systems, or ELSS, are a common term for equity mutual fund programs. Investments in an ELSS are deductible from your taxable income under Section 80C of the Income Tax Act of 1961. While there are no upper limits on ELSS investments, the maximum deduction allowed by Section 80C is only Rs 150,000. The ELSS funds are subject to the three-year lock-in term. There are no allowed withdrawals or redemptions during the lock-in period.

Because there is less redemption pressure in ELSS than in other open-ended plans, fund managers may stay to their high-conviction stocks, which is why investors gain from the lock-in period. Because ELSS funds are market-linked investments, they are susceptible to market risks. Consult a Mutual Fund Distributor or financial counselor for help with investment decisions. Your investment strategy should be based on your tolerance for risk.

What Justifies Investing in ELSS?

Equity has historically outperformed inflation in terms of return on investment over long periods, notwithstanding its volatility. The Sensex’s 10-year rolling returns from June 1, 2023, to May 31, 2023, showed an average compound annual growth rate of 12.63% (source: AMFI Best Practice guidelines 109). The CPI inflation rate was 5.1% on average during that period (source: World Bank, Forbes, as of November 30, 2023).

In addition to assisting, you in lowering your tax liability, tax planning should help you achieve your long-term financial goals. ELSS fund managers want to beat the market benchmark index to produce alpha for investors. Wealth can be generated via ELSS investments over long investment periods. (Disclaimer: Stock investments may be impacted by market risks).

ELSS has more liquidity than other 80C investing options.

For ELSS, the lock-in period is merely three years. For a minimum of five years, there is no liquidity available for additional 80C assets. Liquidity needs to be carefully considered while making investments.

An ELSS is among the most tax-efficient investment options available under Section 80C. Up to Rs 100,000 in a financial year, capital gains are tax-free; above that, they are liable to 10% tax (plus any applicable surcharge and cess).

Who should invest in ELSS Mutual Fund Schemes?

>Investors who are looking to earn from lower taxes and long-term capital gains.

>Investors with somewhat to extremely high-risk tolerances.

Consult your financial advisor if you are unsure about your level of risk tolerance.

Important:

Investors should invest as soon as possible to take advantage of the tax benefits for the current financial year, after first determining whether ELSS is the right product for their tax planning needs by speaking with financial advisors or mutual fund distributors.

To find the best ELSS fund visit our premium research tool fabricated with thousands of data points. https://swarajfinpro.com/